In what follows I'll offer a brief summary of the post (he writes longer blog posts than I do!) and a few points of criticism as well. The criticisms offered, I think, will be in the spirit of Jesse Livermore's criticisms of other metrics which attempt to predict future returns (see here).

The Model

So let's start by looking at the model.

Livermore notes returns over a 10 year horizon will be determined by the dividends and price appreciation. And the price appreciation will actually have a large impact on returns. So what actually determines prices?

Livermore's theoretical model relates prices both to the supply of assets and the allocation of said assets.

Livermore considers three broad categories: cash, bonds and stocks. Investors can choose to allocate an amount to each. Those allocations will influence the prices of those assets. For example, if more people want bonds, that will increase the overall demand for bonds and thus raise prices (lowering future bond returns).

Likewise, we also have to factor in the supply of each asset. If investors want to allocate more to bonds, there needs to be bonds available for purchase.

In spite of all of that, the practical model is simply this: Average Investor Equity Allocation.

So if we sum up all of the investments (cash, bonds and stocks) and look at what percentage of those are invested in stocks, we get Livermore's metric.

In addition, he shows how this can be calculated from FRED:

Here's the Average Investor Equity Allocation.

Here are all of the components.

The interesting thing is that it actually does a better job of predicting future returns than more traditional metrics such as CAPE:

I suspect we're using different series for 10Y returns but both look fairly similar. My r2 figure is a tad lower than his but it's still a much better fit than other models.

So where is the model predicting returns will be? It's predicting returns of about 7.3%. Standard deviation of the error terms is about 1.7% so (assuming this continues to work in the future) it may still be off a bit. But that's still not a horrible prediction.

The Boomer Effect: Demographics and Stock Prices

I want to take a bit of a detour a minute to another phenomenon that is not talked about too much which has to do with demographics. The main group that has been exhibiting influence on markets (and will continue to do so for a few more years) are the baby boomers. The baby boomers are roughly those born in the post-war period (say, between 1945-1965).

An article at the Fed by Zheng Liu and Mark M Spiegel called Boomer Retirement: Headwinds for U.S. Equity Markets? attempts to explore this issue.

The idea is quite simple. Consider a "typical" American. A person in her 20's will have just recently graduated and is now working in an entry level job (not making much money). Any extra money she has will likely go to family starting related expenses (perhaps a down payment on a home).

Fast forward to a person in her 40's. Now she's making good money. The kids may have already graduated so there's a shift now to focus on saving for retirement. This means she's buying stocks.

Fast forward again to a person in her 60's. Now she's either going into retirement or will be soon. The expectation is that she has been shifting assets from stocks to bonds and cash.

So the author's propose what they call the MO ratio which is the ratio of the people in their 40's versus the ratio of people in their 60's.

The interesting thing is that this ratio correlates well with PE ratios (I followed the authors of the article in looking at the power law, e.g. comparing the natural logs of both variables):

Since this MO ratio is expected to decline as the boomers get older the conclusion that is drawn in the article is that PE ratios will subsequently contract putting downward pressure on stock prices and subsequently stock returns.

Why would Average Equity Allocation Fail to Predict Future Stock Returns?

I want to move now to offer a bit of a critique. One problem we always face with something like this is the problem of induction: will future results be like past results? Or to put it another way, will this model continue to predict well in the future?

So let's consider some reasons why this model would not work well.

1) Earnings Growth

One of the implicit assumptions in the model is that earnings growth is roughly the same for all periods. If however, earnings growth (hence, dividend growth) is larger (smaller) that would easily have a positive (negative) effect on subsequent returns.

2) Final Average Equity Allocation

One thing we should expect is that since returns ultimately depend, not only on the price paid but also, on the final price, we should expect that the final average equity allocation will effect returns. If there's a large increase or decrease in the allocation that should result in higher or lower subsequent returns.

Here's what the subsequent difference in 10Y Average Equity Allocation looks like:

Periods such as 1950's, 1980's and 1990's saw a large shift into equities. The period of about 1965-1975 as well as the period following the dot com burst saw a large shift out of equities. The expectation would be that the model should not predict as well in these places.

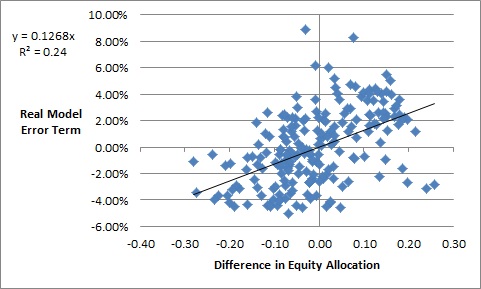

3) Inflation

One real question is why this model does a good job of predicting nominal returns. Should it also not predict real returns? And which should it do better?

As a matter of the historical record, it actually does a better job of predicting nominal returns. But I see no theoretical reason why it should. Here's what the model looks like for real returns:

The period of the late 70's to early 80's was a period of high inflation in the US. But the nominal prediction is actually fairly decent whereas the real prediction didn't work so well. Why is this?

Putting It All Together

I believe that these three factors (as well as many more) may be counteracting against each other. In particular, the period of the late 60's to early 70's was a period in which equity allocations were in decline (having a negative impact on returns) but inflation was high (having a positive impact on nominal earnings) and the two effects negated each other to some extent. So the nominal model predicted well and the real model did not do so well.

In the period from the late 80's to early 90's, both models had off predictions. Both nominal and real returns were higher than the model predicted and that appears to be largely due to the increase in equity allocations that occurred over this period (having a positive effect on returns).

In fact, a portion of why the real model fails where it does can be explained by the change in Average Equity Allocation:

Can We Predict Future Equity Allocations?

And the fact of the matter is that none of this would really matter unless we can actually predict future equity allocations. And that's actually the reason I took that little detour into the boomer effect. Because that MO ratio is actually not a bad predictor of future equity allocaitons:

As more boomers enter retirement we should see allocations moving away from stocks.

So I believe there is good reason to suspect that (1) future equity allocation will decline and, as a result, (2) actual returns will be lower than the model is currently predicting.

A Couple Misc. Comments/Criticisms

So there are two additional points from Jesse Livermore's article I want to touch on that I think are important.

Investing and Time Horizons

Here's the first part which I'll quote verbatim:

Many investors don’t like the fact that price drives total return. If price drives total return, it follows that total return is a function of the shifting sentiment, preferences and expectations of other people–those who make up the market and “vote” on what the price will be. Investors don’t want their returns to be subject to the arbitrary “vote” of other people, and so they pretend that as stock market speculators they are actually genuine businessmen who “buy” and “own” companies to hold forever. They tell themselves that their returns will somehow emerge directly from the cash flows of the underlying businesses, regardless of what the market decides to do with price.I think this is a fair point regarding the fact that, say, on a 10 year horizon the final price matters a great deal and therefore things like investor sentiment matters.

This point of view ignores the fact that it takes decades to recoup an equity investment via dividends, the only cash flows that are ever are actually paid out to buy-and-hold investors. To claim a return on a stock in any other context, an investor needs someone to sell it to. The price that other people are wiling to pay is therefore important–supremely important. Rather than resist this fact puristically, our responsibility as investors is to accept it and work within it, by understanding the behavioral propensities of our fellow market participants, and getting in front of emerging trends in how they choose to allocate their wealth.

Where I disagree is that investment proper, in my view, requires asset-liability management.

If I'm saving for a one year time horizon I wouldn't go out and buy a 10 year bond. Likewise, if I'm saving for only 10 years, stocks may be too long-term of an investment class to purchase on a short time horizon.

In fact, as John Hussman notes, we can approximate the duration of a stock as being the price to dividend ratio. With dividend yields around 2%, that puts the duration of the stock market at around 50 years. So you really need a longer time horizon to invest in stocks at present. Otherwise you are speculating, to some extent, on what people are willing to pay for it in the future.

Comparing Returns to Alternatives

This is just a minor nitpick but I think it's important. I agree with Jesse Livermore that when looking at stocks and whether or not they are over/undervalued one has to look at them compared with alternative investments. In the current low interest rate environment we should not expect stock returns to get the 8-10% they have historically achieved.

But I think this should be put in context to all alternatives. Investment grade corporate bonds offer quite attractive returns compared with treasuries. And whatever model we're looking at, there is not much room for error as to whether or not stocks will outperform these instruments.

On a long-term horizon, we can achieve somewhere above 5% on long-term investment grade corporate bonds (see here. The yield would have to be adjusted for losses due to default but that would likely be very low for investment grade corporate bonds).

Quick Concluding Comments

I think this is an interesting approach and it certainly has a nice fit. I think there is still room to argue that not only may returns may turn out to be lousy but they may ultimately end up underperforming investment grade bonds. A minor correction may be sufficient to change that dilemma.

Of course buying the S&P 500 is only one investment strategy. There are plenty of individual stocks that have far better return characteristics as well as stocks from other countries to dig through.

Is it appropriate that Average Investor Equity Allocation disregards real estate as an asset allocation class?

ReplyDeleteHi Stu,

ReplyDeleteIn detail, probably not. But it might not make a huge difference.

One of the components in his calculation was Households and Nonprofit Organizations; Credit Market Instruments; Liability.

That shows up on line 40 here.

According to how it's calculated, it factors in mortgage liabilities. (It's the sum of lines 41-46 on the other table.)

That would at least partly account for real estate. I don't see anything that would suggest equity is factored in (except for real estate owned by corporations.) So at the very least household and nonprofit real estate equity is not in the equation as far as I can tell. If there were a big move in real estate equity that might affect the model.